Every commercial real estate deal that gets financed is, at its core, a stack of capital. A sponsor doesn't write one check from one source for the full purchase price. Instead, the deal is funded by layers: a senior loan from a bank or agency lender, sometimes a mezzanine slice on top of that, sometimes preferred equity, and finally the common equity that sits in the riskiest position but earns the upside if the property performs. The way those layers are sized, priced, and structured is called the capital stack, and learning to read one is the difference between a deal that pencils and one that gets stuck in committee.

For sponsors, the capital stack is a design problem. The right combination of debt and equity unlocks higher returns on the common equity, lets you close on bigger deals without putting more of your own money in, and keeps the property solvent through downturns. For brokers and investors, the capital stack is a diagnostic. It tells you who has what risk, who gets paid first if things go sideways, and where the deal is over- or under-leveraged.

This guide walks through what the capital stack is, what each layer looks like in practice, how to think about cost of capital across the stack, the most common stack structures, and the tradeoffs sponsors weigh when they're stacking capital on a real deal. If you'd rather skip the manual work and get matched with lenders and capital providers whose criteria your deal already fits, Lev does that automatically.

What is the capital stack?

The capital stack is the ordered hierarchy of every dollar that funds a CRE deal, ranked by the priority each provider has on the property's cash flow and, in a worst case, the property itself. The bottom of the stack gets paid first and bears the least risk. The top of the stack gets paid last and bears the most. Returns on each layer are priced to match that risk, so the highest-priced capital sits at the top.

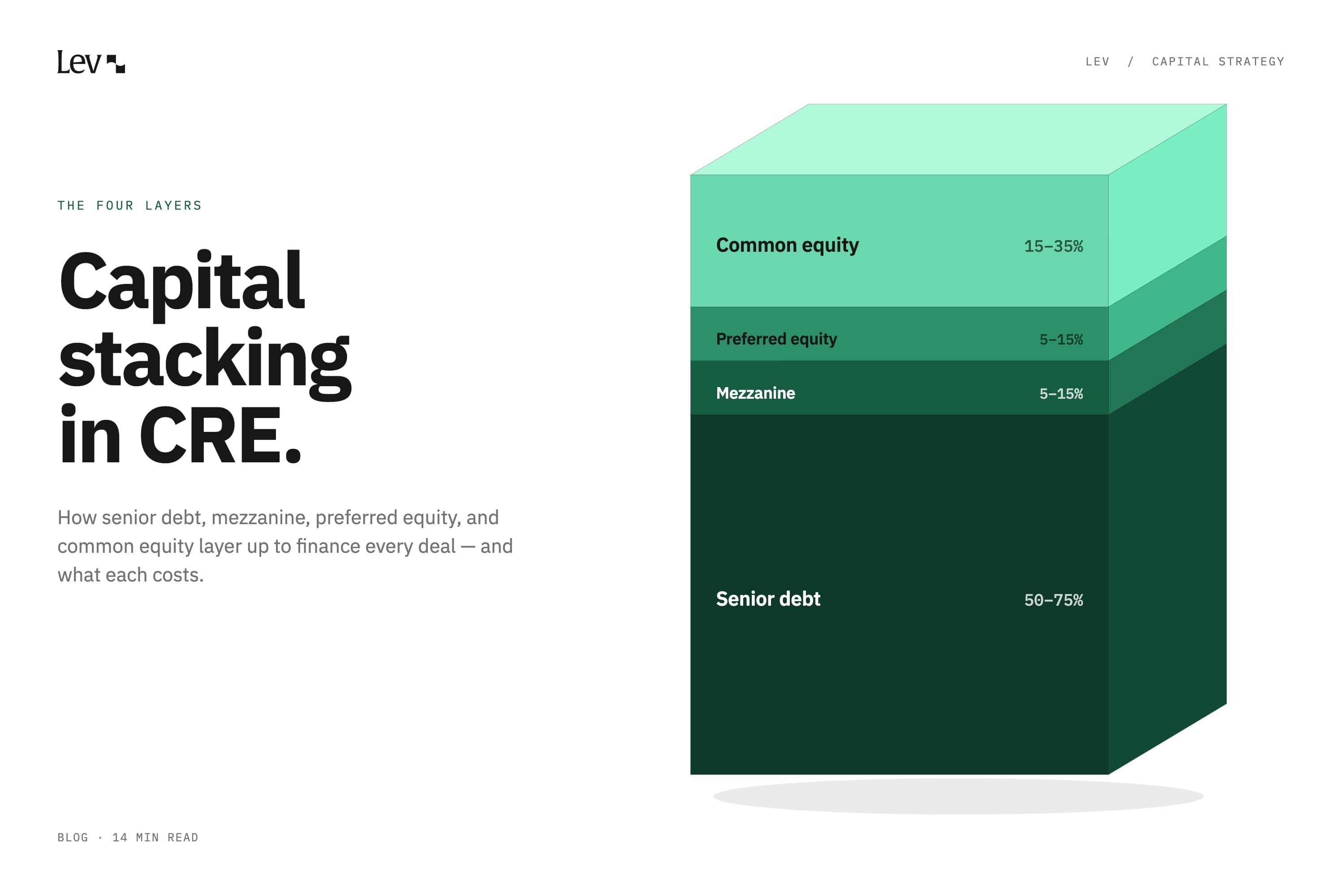

A typical stack reads from bottom to top like this:

- Senior debt: the largest layer and the first to get paid. Usually 50 to 75% of the project's capitalization.

- Mezzanine debt or subordinate debt: a smaller slice that sits behind the senior loan. Typically 5 to 15% of the stack.

- Preferred equity: equity with a fixed payment priority over common equity but no foreclosure rights. Often 5 to 15%.

- Common equity: the sponsor's and investors' equity. The last to get paid and the first to lose value if the deal underperforms. Usually 15 to 35%.

The stack doesn't have to include all four layers. A simple deal might be 65% senior debt and 35% common equity. A more aggressive deal might use all four layers to push leverage to 90% or higher. The right structure depends on the property, the business plan, and what the sponsor is trying to optimize for.

A useful way to picture the stack: senior debt is the foundation, common equity is the roof, and everything else is what fills the space between. The further up you go, the higher the expected return, but also the higher the chance you walk away with nothing if the property underperforms.

Senior debt: the foundation

Senior debt is the largest and lowest-cost layer of almost every capital stack. The senior lender has a first-priority lien on the property, which means if the borrower defaults, the senior lender can foreclose and recover from the sale of the asset before any other capital provider gets a dollar. Because the senior position is the safest, it's also the cheapest.

Common senior lenders include banks, life insurance companies, debt funds, CMBS conduits, agency lenders (Fannie Mae and Freddie Mac for multifamily), and SBA lenders for owner-occupied properties. Each has its own appetite, leverage limits, and underwriting style, which is why broker-led financing typically involves shopping multiple senior lenders to find the best fit.

Senior debt is usually sized by two constraints: loan-to-value (LTV) and debt service coverage ratio (DSCR). LTV measures the loan amount against the property's appraised value, and stabilized senior loans typically top out at 65 to 75% LTV. DSCR measures the property's cash flow against its annual debt service, and most senior lenders want at least 1.20 to 1.30. Whichever constraint is tighter caps the loan, and on most deals DSCR caps the loan before LTV does.

Pricing for senior debt typically lands in the range of SOFR plus 175 to 300 basis points for floating-rate bank loans and 5 to 7% for fixed-rate CMBS or life company loans, depending on the rate environment, the property type, and the sponsor's profile. Loan terms run 5, 7, or 10 years for permanent loans, with amortization usually based on a 25 or 30-year schedule and a balloon at maturity.

For a deeper dive on how senior lenders size and price loans, see Lev's guide to commercial bridge lenders and the LTV ratio walkthrough.

Mezzanine debt: the middle layer

Mezzanine debt sits above the senior loan and below all equity. The mezzanine lender does not have a first lien on the property. Instead, the mezzanine loan is secured by a pledge of the equity interests in the entity that owns the property. If the borrower defaults on the mezz loan, the mezz lender can foreclose on the ownership interests and step into the equity position, but the senior loan stays in place above it.

Mezzanine financing is typically used to bridge the gap between senior debt and the equity a sponsor is willing or able to write. If a senior lender will only go to 65% LTV but the sponsor can find mezz at another 10%, that's an extra $1 million on a $10 million deal that doesn't have to come out of the sponsor's pocket. The cost is meaningful: mezz coupons typically run 9 to 14%, sometimes higher in tighter credit markets.

For more on mezz structures, including the difference between mezz and preferred equity, see Lev's mezzanine debt explainer and the preferred equity vs mezzanine debt comparison.

Mezzanine debt almost always has a current-pay interest component and, often, an accrual component that compounds and is paid at exit. Some mezz lenders also negotiate for a small equity kicker or warrant. Mezz lenders typically want intercreditor agreements with the senior lender that govern what happens in default, and the negotiation of those agreements is one of the most lawyer-heavy parts of any deal that includes mezz.

Preferred equity: equity with priority

Preferred equity is structured as an equity investment but functions like a hybrid of debt and equity. The preferred equity holder gets a fixed return (sometimes called a preferred coupon or pref rate) paid before common equity sees any distribution. Most pref equity has a target return in the 9 to 13% range, similar to mezz, but the legal structure is different. Pref equity is not a loan, so the pref holder does not have foreclosure rights if payments are missed. Instead, the pref holder typically has the right to take over management of the asset under a change-of-control provision, replace the general partner, or force a sale.

Preferred equity comes in two main flavors:

Hard pref: behaves more like debt. Fixed coupon, must be paid before common equity, often has a maturity date. Sometimes the senior lender will require it to be re-characterized as equity for loan covenant purposes, but the cash flow rights look like a loan.

Soft pref: behaves more like equity. The pref holder gets a preferred return, but if cash flow falls short, the unpaid pref simply accrues and is paid at exit. There's no event of default, no acceleration, no enforcement action.

Sponsors often use pref equity instead of mezz when the senior lender's loan documents prohibit subordinated debt or when there's a strategic reason to keep the capital stack on the equity side of the line. For the investor providing pref, the upside is a higher return than senior debt and less downside risk than common equity, but you give up the chance to participate in the deal's full upside.

Common equity: the last to get paid

Common equity sits at the top of the stack. It's the last layer to receive cash flow, the last to recover principal at a sale, and the first to absorb losses. In exchange for that risk position, common equity earns the residual: anything left over after senior debt, mezz, and pref equity have been paid is split among the common equity holders.

In a sponsored deal, common equity is usually split between the sponsor (the "GP," or general partner) and the limited partners ("LPs") who invest passively. The split is governed by a waterfall, a contractual structure that defines how cash gets distributed at different return thresholds. A typical multifamily waterfall might look like:

- 100% of cash flow to LPs until they earn an 8% preferred return on their invested capital

- Then a 70/30 split (LPs get 70%, sponsor gets 30%) until LPs earn a 15% IRR

- Then a 50/50 split above 15%

The mechanics of the waterfall let the sponsor earn meaningfully more than their pro-rata share of the equity, but only if the deal performs above the preferred return. If the deal underperforms, the sponsor's promote shrinks or disappears.

Common equity is the most expensive capital in the stack because it bears all the risk. Underwritten return targets are usually 15 to 22% IRR for value-add and core-plus deals and higher for opportunistic or ground-up development.

For more on the GP/LP split and how waterfalls work, see General partner in commercial real estate and the joint venture equity guide.

How sponsors think about cost of capital across the stack

Each layer in the stack has a different cost, and the weighted average of all those costs is the deal's blended cost of capital. A sponsor designing a stack is balancing two things at once: getting the highest leverage they can (which usually amplifies returns to common equity) without driving the blended cost so high that the deal stops working.

A simplified example. Consider a $10M deal with the following stack:

- Senior debt: $6.5M at 6.5% = $422,500/year

- Mezz: $1M at 11% = $110,000/year

- Pref equity: $0.5M at 10% = $50,000/year

- Common equity: $2M

If the property's NOI is $750,000/year, debt service plus pref equity coupon is $582,500. That leaves $167,500 of cash flow to common equity, or 8.4% cash-on-cash on the $2M of common equity, before any promote. The same property financed with just $6.5M senior debt and $3.5M common equity would generate $327,500 of cash flow to common, or 9.4% cash-on-cash, but on a much larger equity check. The leverage of mezz and pref lets the sponsor close the deal with less of their own money in.

This is the central trade-off in capital stack design: how much expensive capital you add to get the equity check small enough to attract LPs and large enough to amplify returns, without crossing the line where you starve cash flow.

Common capital stack structures by deal type

The "right" stack depends heavily on what kind of deal you're financing.

Stabilized multifamily

The cleanest stack in CRE. Often just two layers: agency or bank senior debt at 65 to 75% LTV, and common equity for the rest. Mezz is uncommon on stabilized multifamily because the agencies don't allow subordinate debt. If extra leverage is needed, preferred equity is the standard tool.

Value-add multifamily

Senior debt (often a bridge loan during the value-add period, refinanced into agency permanent at stabilization), sometimes mezz on top, common equity. Total leverage often 75 to 85% LTC at acquisition.

Office, retail, industrial (stabilized)

Senior debt from CMBS, life company, or bank at 60 to 70% LTV. Sometimes pref equity. Common equity for the balance. Mezz appears more often in office and industrial than in multifamily.

Ground-up development

Construction loan (interest-only, dollars drawn as project milestones are hit) at 55 to 65% LTC. Sometimes mezz construction. Sponsor equity for the balance. Often a pre-negotiated permanent loan ("forward take-out") for stabilization.

Bridge / repositioning

Senior bridge loan from a debt fund or specialty lender at 65 to 75% LTV. Sometimes preferred equity. Common equity for the gap. Pricing on bridge senior debt is often 200 to 400 basis points over a floating index.

SBA owner-occupied

SBA 504 deals have a built-in stack: 50% from a conventional senior lender, 40% from the SBA 504 CDC, 10% from the owner. The 504 piece is technically a second mortgage but functions like patient long-term debt.

How to read a stack on a deal you're underwriting

When a sponsor sends you a capital stack chart or an OM with one, here's what to check:

Are the layers sized realistically? A 78% LTV senior loan on an office property in a soft market is almost certainly a stretch. Sanity-check each layer against what's actually available in the current market for that property type.

Does the cash flow service all the layers? Compute NOI, subtract senior debt service, mezz coupon, and pref coupon. What's left for common equity, and is the cash-on-cash return reasonable?

What's the intercreditor structure? If there's mezz or pref, who controls decisions if things go sideways? Who can force a sale? What are the cure rights?

What's the refinancing risk? Most permanent CRE loans have a balloon at maturity. Will the property's value at maturity support a refi at the new prevailing rates? Stress-test the exit refi at 200 basis points higher than today's rates.

Where's the sponsor's skin in the game? A sponsor putting in less than 5 to 10% of the equity typically signals a thinly capitalized deal. Most institutional LPs want to see at least 10 to 20% sponsor co-investment in the common equity.

For a more complete diligence framework, see Lev's CRE due diligence guide.

When the capital stack breaks

The capital stack works as long as the property generates enough cash flow and value to service all the layers. When it doesn't, the stack starts to break from the top down.

The first to lose value is common equity. If cash flow drops or the property's value falls below the senior loan balance plus mezz plus pref, the common equity is wiped out before any senior layer takes a hit. Sponsors with negative-equity properties often face the "rescue capital" decision: bring in additional equity (almost always at punitive terms) or hand the keys back to the lender.

The second layer at risk is preferred equity, and if the situation gets worse, mezzanine debt. In a default scenario on a mezz loan, the mezz lender typically forecloses on the equity interests and takes over as the new common equity owner, still owing the senior debt above them. Mezz lenders price their loans assuming this can happen.

Senior debt almost always recovers something, even in a foreclosure, because the senior position is collateralized by the asset itself. The senior lender's loss is the difference between the loan balance and the foreclosure sale proceeds, and on most properties that's a partial loss, not a total wipeout.

Understanding which layer absorbs losses first is essential for both sponsors and investors. The stack isn't just an abstraction; in a downturn, the order matters.

How Lev helps sponsors design and fund the stack

For sponsors, building a capital stack is half analytical and half a sourcing problem. You need to know what structure works for your deal, and then you need to find the lenders and capital providers who will actually do it. Lev's platform speeds up both halves.

Sponsors enter the deal once: property type, location, business plan, projected NOI, sources and uses, sponsor profile. Lev matches that profile against the criteria of senior debt lenders, mezz providers, and pref equity sources, surfaces the ones whose box the deal fits, and lets the sponsor reach out to multiple capital sources in parallel rather than sequentially. The result is more competing offers and a stronger final stack.

Brokers using Lev work the same way: enter the client's deal, see the menu of senior debt options at different leverage points, and overlay mezz or pref where it makes the deal work. The platform's market data gives a real-time view of where pricing is for each layer of the stack, which makes the sponsor's first conversation with capital sources much more informed.

Frequently asked questions

What's the difference between a capital stack and a debt stack?

A debt stack refers only to the debt layers (senior debt plus any subordinate debt like mezzanine). A capital stack includes everything: senior debt, subordinate debt, preferred equity, and common equity. The capital stack is the full picture of how a deal is financed; the debt stack is the financed-with-debt portion.

Is mezzanine debt the same as a second mortgage?

No, though they sometimes get conflated. A second mortgage is a second-priority lien on the property itself. Mezzanine debt is not secured by the property at all; it's secured by a pledge of the equity in the entity that owns the property. The legal foreclosure path is different (a UCC foreclosure on the equity interests rather than a real estate foreclosure on the property), and the intercreditor relationship with the senior lender is more flexible.

What's a typical loan-to-cost (LTC) for a CRE deal with mezz?

For value-add or bridge deals with senior plus mezz, total LTC commonly runs 75 to 85%. Senior debt provides 60 to 70% LTC, and mezz fills the gap to the target. For ground-up construction, total LTC with senior and mezz can reach 80 to 85% in strong markets.

Why would a sponsor use preferred equity instead of mezzanine debt?

A few reasons. First, the senior loan documents may prohibit subordinate debt but allow preferred equity, since pref is technically an equity instrument. Second, pref doesn't add another lien to the property or require an intercreditor agreement, which can streamline closing. Third, in a downturn, pref equity that misses a payment typically accrues, rather than triggering a default event the way mezz would. The trade-off is that pref equity usually has less downside protection for the investor than mezz, so it sometimes prices a bit higher.

What's a promote, and how does it interact with the capital stack?

A promote is the sponsor's share of profits above a preferred return threshold paid to the LPs. It sits inside the common equity layer of the stack, not as a separate layer. Promotes typically kick in after the LPs earn their preferred return (often 7 to 9%) and are stacked through additional return tiers (a "waterfall"). The promote is how sponsors earn outsized returns on small co-invest checks if the deal performs.

How does the capital stack change in a higher rate environment?

When senior rates rise, the loan amount that DSCR will support shrinks, so the senior layer of the stack gets smaller relative to the deal size. Sponsors typically respond in one of three ways: add more common equity (which lowers returns to LPs), add mezz or pref to fill the gap (which raises blended cost of capital but preserves equity returns), or restructure the business plan to defer some capital improvements until refi.

Can a deal have multiple senior lenders?

Sometimes, in a syndicated senior loan where multiple lenders share the senior position pari passu (equal priority). Common in larger deals where no single lender wants the full exposure. For smaller deals, the senior is typically just one lender.

How big should the sponsor co-invest be?

Most institutional LPs want to see the sponsor putting in 5 to 20% of the common equity. Less than 5% raises alignment concerns. More than 20% sometimes signals that the sponsor couldn't raise outside capital. The right number varies by sponsor track record, deal size, and investor base.

What happens to the capital stack at refinance?

The senior loan is replaced with a new senior loan, often at a different size, rate, and term. Mezz and pref are usually paid off in full at refi (and the providers expect that). Common equity stays in place but may receive a cash distribution if the new senior loan upsizes the total debt on the property. Refinancing is often where the sponsor returns initial LP capital and resets the stack for the next holding period.

Is there a "best" capital stack?

No. The best stack is the one that lets the deal close on terms the sponsor and investors are comfortable with. A heavily levered stack maximizes equity returns when things go right and accelerates losses when they don't. A conservatively levered stack does the opposite. Most sophisticated sponsors target a stack that pencils to a target return at a reasonable downside, with enough margin to survive a downturn.

The takeaway

The capital stack is the architecture of every CRE deal. Senior debt is the foundation, common equity is the residual, and mezzanine and preferred equity fill the space between. Designing the stack is about balancing leverage against blended cost of capital, and reading a stack is about understanding who has what risk and what gets paid first.

For sponsors, the right stack is the one that closes the deal at a return that compensates everyone fairly for the risk they're taking. For brokers and investors, the stack is the cleanest single picture of what a deal really looks like. If you'd rather skip the spreadsheets and get matched directly with senior lenders, mezz providers, and preferred equity sources whose criteria your deal fits, start with Lev and get 3,000 free credits to evaluate the platform.